v1.2.0

Statistical Indicators

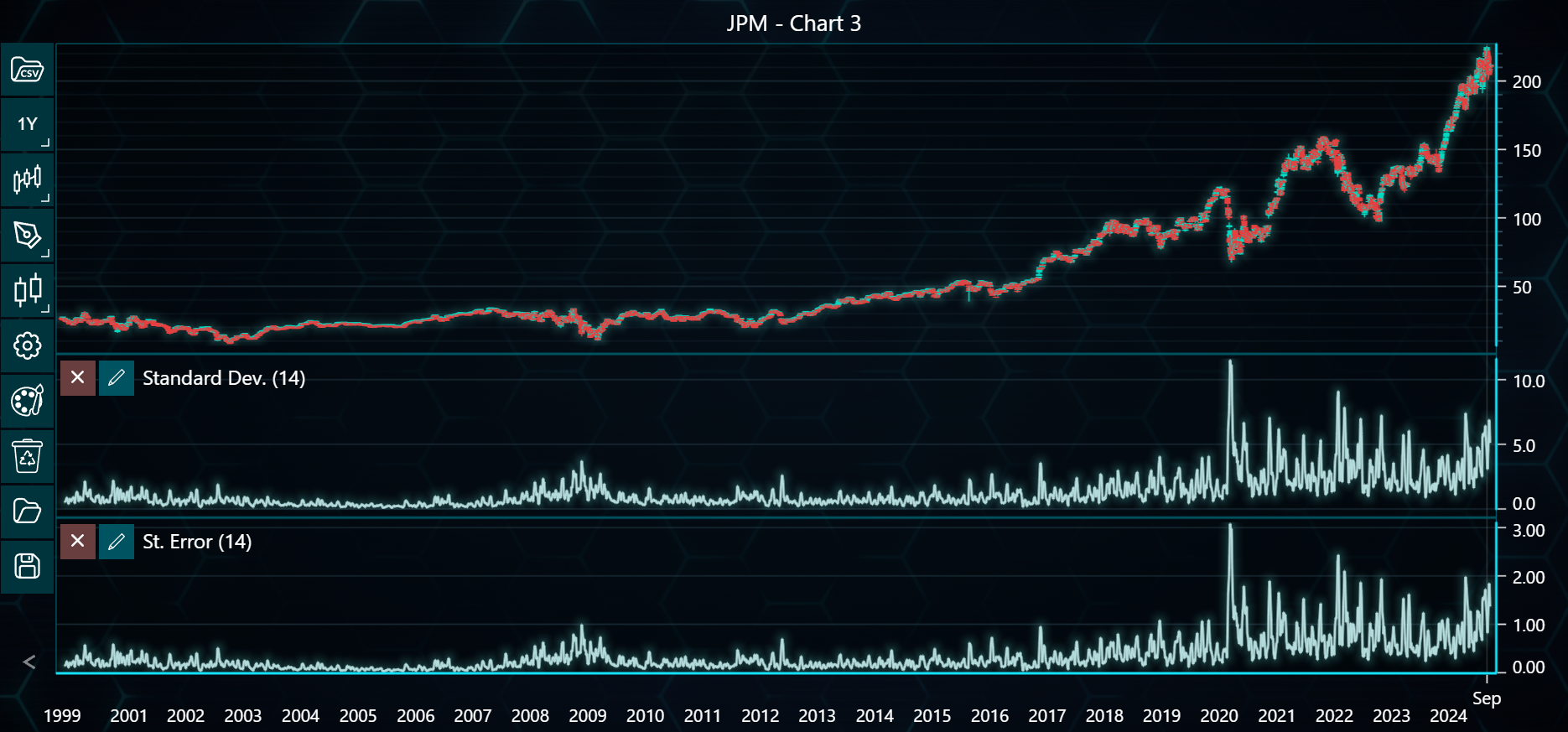

This example demonstrates how to use statistical indicators such as kurtosis, skewness, standard deviation, and correlation coefficients across multiple datasets (BAC, GS, JPM) in LightningChart Python Trader. Full code and datasets are included for download.

Download 'Bank of America Corp (BAC).csv'

Download 'The Goldman Sachs Group (GS).csv'

Download 'JPMorgan Chase & Co (JPM).csv'

from lightningchart_trader import TAChart

from lightningchart_trader.helper_routines import convert_to_xohlc

LICENSE_KEY_PATH = 'license_key.txt'

BAC_DATA_PATH = 'Bank of America Corp (BAC).csv'

GS_DATA_PATH = 'The Goldman Sachs Group (GS).csv'

JPM_DATA_PATH = 'JPMorgan Chase & Co (JPM).csv'

# Load the license key

license_key = open(LICENSE_KEY_PATH).read()

# Initialize Trading chartlications

chart1 = TAChart(license_key=license_key)

chart2 = TAChart(license_key=license_key)

chart3 = TAChart(license_key=license_key)

# Load CSV files into TAChart instances

chart1.load_csv(csv=BAC_DATA_PATH, dataset_name='BAC Data - Chart 1')

chart2.load_csv(csv=GS_DATA_PATH, dataset_name='GS Data - Chart 2')

chart3.load_csv(csv=JPM_DATA_PATH, dataset_name='JPM - Chart 3')

xohlc_data_BAC = convert_to_xohlc(BAC_DATA_PATH)

xohlc_data_GS = convert_to_xohlc(GS_DATA_PATH)

xohlc_data_JPM = convert_to_xohlc(JPM_DATA_PATH)

# Configure indicators for each chart

chart1.add_kurtosis()

chart1.add_median_price()

chart2.add_skewness()

cc1 = chart2.add_correlation_coefficient()

cc2 = chart2.add_correlation_coefficient()

chart3.add_standard_deviation(period_count=14)

chart3.add_standard_error(period_count=14)

# Assign Correctly Formatted Data to Correlation Coefficients

cc1.set_dataset(xohlc_data_BAC)

cc1.set_symbol('BAC')

cc1.set_line_color('#4444DD')

# cc2.set_dataset(jpm_data)

cc2.set_dataset(xohlc_data_JPM)

cc2.set_symbol('JPM')

cc2.set_line_color('#DD4444')

# Collect all chart instances in a list

charts = [chart1, chart2, chart3]

# Open all charts

for chart in charts:

chart.open()