LightningChart JS TraderA Complete Guide to Correlation Coefficient Statistics

ArticleLearn about Correlation Coefficient Statistics as a method to measure the relationship between variables

Written by a human | Updated on April 24th, 2025

Introduction to Correlation Coefficient Statistics

In financial analysis, understanding the relationship between different variables is crucial for making informed decisions. The correlation coefficient statistics is one of the most widely used methods to measure this relationship, particularly in markets that rely on the interplay of different assets, such as stock trading. In this article, we will dive into the correlation coefficient in statistics, its calculation, and how it can be used effectively in financial contexts.

What is a Correlation Coefficient Statistics?

The correlation coefficient is a statistical measure that indicates the strength and direction of a linear relationship between two variables. This coefficient ranges from -1 to +1:

- A correlation coefficient of +1 indicates a perfect positive linear relationship.

- A correlation coefficient of -1 indicates a perfect negative linear relationship.

- A value of 0 suggests no linear correlation between the variables.

In financial analysis, traders often rely on this coefficient of correlation to understand how two assets move in relation to each other. For instance, the correlation coefficient statistics between two stocks may reveal whether their prices tend to move in the same or opposite directions.

Strong Positive and Negative Correlation Coefficient

A strong positive correlation (values close to +1) suggests that as one asset’s price increases, the other asset’s price is also likely to increase. In contrast, a strong negative correlation (values near -1) suggests that one asset’s price increases while the other’s decreases. Both types of relationships provide valuable insights for portfolio diversification and risk management in trading.

Types of Correlation Coefficients

Several types of correlation coefficients statistics are used in statistical analysis, depending on the data and the relationships being measured. The three most commonly used in financial contexts are:

- Pearson Correlation Coefficient: This is the most widely used correlation coefficient in statistics and measures the linear relationship between two variables.

- Spearman Rank Correlation Coefficient: Used when data does not necessarily follow a linear relationship but can be ranked.

- Kendall Correlation Coefficient: Measures the ordinal association between two measured quantities, often used in cases with small sample sizes or when distributions are not normal.

Each of these types of correlation coefficient statistics has its own specific use cases in finance, depending on the data’s nature and the intended analysis.

How does the Correlation Coefficient work?

The formula for correlation coefficient in statistics is derived from covariance and standard deviations. Specifically, the Pearson correlation coefficient.

Where:

- Cov(X, Y) is the covariance of the variables X and Y,

- σx and σy are the standard deviations of X and Y, respectively.

This correlation coefficient formula in statistics expresses how the variables co-vary with each other in relation to their standard deviations. In trading, this helps to quantify whether two assets tend to move together or apart.

Understanding Covariance

Covariance is a measure of how much two random variables change together. If the variables tend to increase or decrease simultaneously, the covariance will be positive, suggesting a positive relationship. If one increases while the other decreases, the covariance will be negative, indicating a negative relationship. The formula for covariance is given by:

Where:

- Xi and Yi are the individual observations for the variables X and Y,

- X̅and Y̅ are the means of the respective variables,

- ? is the number of data points.

In the covariance formula, each term measures the deviation of a data point from the mean for each variable. The product of these deviations is then summed across all data points and divided by the number of observations. Positive covariance means that when one variable is above its mean, the other tends to be above its mean as well (and vice versa for negative covariance).

However, covariance alone is not sufficient for interpreting the strength of the relationship between variables, as it depends on the scale of the data. Therefore, the Pearson correlation coefficient normalizes this measure by dividing it by the standard deviations of both variables.

Standard Deviation

The standard deviation quantifies the amount of variation or dispersion in a set of values. In the correlation formula, ensures that the covariance is standardized, making the measure comparable across different datasets.

The formula for the standard deviation of a variable X is:

The same formula applies for Y, except with the values of Yi and the mean Y̅.

Deriving the Pearson Correlation Coefficient Formula

Combining the covariance and standard deviation formulas, the Pearson correlation coefficient can be written as:

This formula computes the correlation coefficient by summing the products of the deviations of each variable from its mean and dividing by the product of their standard deviations. The result is a unitless measure that indicates the degree of linear relationship between the variables, regardless of their scale.

Interpreting the Pearson Correlation Coefficient

The Pearson correlation coefficient gives insight into the strength and direction of the linear relationship:

- r = +1: Perfect positive correlation, as one variable increases, the other also increases at a constant rate.

- r = -1: Perfect negative correlation, as one variable increases, the other decreases at a constant rate.

- r = 0: No linear correlation, there is no linear relationship between the variables, though a non-linear relationship may still exist.

The value of r near +1 or -1 indicates a strong correlation, while values closer to 0 represent weaker relationships. However, it’s crucial to understand that Pearson’s r only captures linear relationships. It does not indicate the existence or strength of non-linear relationships.

Example:

Let’s consider two assets, Stock A and Stock B, with historical returns over a period. To compute the statistical correlation coefficient, we first calculate the covariance between these two stocks’ returns and their respective standard deviations. By applying the correlation coefficient formula, we can then derive a value that indicates how closely these assets’ prices are related.

For example:

- If r = 0.85, the statistical correlation coefficient suggests a strong positive relationship, implying that as Stock A rises, Stock B tends to rise as well.

- If r = −0.75, it implies a strong negative relationship, meaning that Stock B falls as Stock A rises.

Statistical Tests for Evaluating the Correlation Coefficient:

To assess the statistical significance of the correlation coefficient, financial analysts often use a test statistic for the correlation coefficient based on the t-statistic. The formula for this test is:

Where:

- r is the correlation coefficient,

- n is the sample size.

This t-statistic correlation coefficient test helps analysts determine whether the observed correlation is statistically significant or if it could have occurred by chance.

Additionally, tools like a test statistic correlation coefficient statistics calculator can simplify the process of finding the statistical significance correlation coefficient for various datasets. These tests ensure that traders base their strategies on meaningful correlations, avoiding misleading signals caused by random data fluctuations.

The Role of LightningChart JS Trader in Financial Analysis

Financial analysis involves examining historical data to forecast future trends, make informed decisions, and assess risk. In this domain, applications like LightningChart JS Trader serve a critical role by providing real-time, high-performance data visualization tools that help traders and analysts better interpret complex datasets. It enables traders to track market trends, calculate correlation coefficient statistics using built-in indicators.

The platform’s ability to handle large datasets and real-time updates makes it essential for fast decision-making in dynamic markets. Additionally, its customization options allow users to create tailored charts and apply statistical indicators, enhancing both the precision of analysis and risk management. This tool helps streamline financial analysis and supports more informed, data-driven trading strategies.

Correlation Coefficient Implementation with LightningChart JS Trader

LightningChart JS Trader is an excellent tool for visualizing correlations in financial markets. It allows users to create sophisticated technical indicators, including those based on correlation coefficient statistics, for decision-making in trading. By integrating the correlation coefficient in statistics into the charting library, traders can observe the interplay between assets and evaluate market conditions visually.

Step 1: Get LightningChart JS Trader

To begin, you’ll need access to LightningChart JS Trader. This library provides the tools necessary to create advanced technical indicators, including correlation coefficients. Visit the LightningChart JS Trader page to download the required components and review the documentation.

Step 2: Review the Interactive Example

LightningChart JS Trader includes interactive examples demonstrating how to create custom technical indicators. Start by reviewing the documentation, focusing on integrating the correlation coefficient into your chart setup. The interactive examples will guide you through the process of setting up the correlation coefficient, from importing the necessary modules to modifying the chart settings.

Step 3: Code Explanation

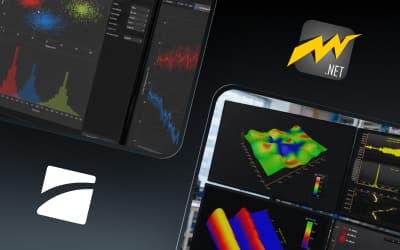

In this step, we will break down the code that creates the chart with the correlation coefficient indicator, as shown in the image, using LightningChart JS Trader. The code demonstrates how to initialize a trading chart, apply the correlation coefficient indicator, and customize its appearance.

Here’s a detailed breakdown of each section:

A. Importing the Required Libraries:

const lcjsTrader = require('@arction/lcjs-trader')

const lcjs = require('@arction/lcjs')

const { Themes } = lcjs- lcjsTrader: This library provides access to the LightningChart JS Trader functionalities, allowing you to create advanced financial charts.

- lcjs: The main LightningChart JS library, used for general charting functionality.

- Themes: A property within lcjs that provides access to pre-built themes. In this case, we are using the darkGold theme to style the chart.

B. Initializing the Trading Chart:

lcjsTrader.trader(TRADER_LICENSE).then(async (trader) => {

// Create a trading chart.

const tradingChart = trader.tradingChart({ loadFromStorage: false, colorTheme: Themes.darkGold })- trader(TRADER_LICENSE): Initializes the LightningChart JS Trader with the provided license key (TRADER_LICENSE). This is required to access the charting functionalities for financial data.

Note you can request a LightningChart JS Trader trial license, which is free.

- tradingChart(): This function creates a trading chart with certain options. In this example:

- loadFromStorage: false: This disables the loading of previously stored chart data from local storage, ensuring a fresh chart setup.

- colorTheme: Themes.darkGold: This applies the darkGold theme to the chart, which influences the background color, grid lines, and other visual elements.

C. Loading Data from a CSV File

// Reading data from a file.

await fetch(`${document.head.baseURI}examples/assets/0000/Alphabet Inc (GOOGL).csv`).then((res) => res.text()).then((text) => {

tradingChart.readCsvString(text, 'Alphabet Inc (GOOGL)')

const dataset = tradingChart.getData(true)

fetch(`${document.head.baseURI}examples/assets/0001/Microsoft Corporation (MSFT).csv`).then((res) => res.text()).then((text) => {

tradingChart.readCsvString(text, 'Microsoft Corporation (MSFT)')

})- fetch(): This function retrieves a CSV file that contains historical pricing data for Alphabet Inc. (GOOGL). The file’s location is specified relative to the base URI of the current document, ensuring accurate fetching of data. This CSV file will be used for plotting GOOGL stock data on the chart.

- readCsvString(): This function reads the CSV data retrieved in the previous step and loads it into the chart. The second argument, ‘Alphabet Inc (GOOGL)’, is used as the label for this dataset in the chart, making it easy to identify GOOGL’s stock data.

- getData(): This method retrieves the current dataset from the chart. The true argument ensures that the method returns all data associated with the loaded dataset (in this case, the GOOGL stock data).

- fetch() (second instance): This second call to fetch() retrieves a separate CSV file for Microsoft Corporation (MSFT), containing its historical stock price data. The purpose is to load multiple datasets on the same chart.

- readCsvString() (inside the second fetch): Similar to the first readCsvString(), this one processes the MSFT data and labels it accordingly, allowing the chart to display stock data for Microsoft alongside Alphabet Inc.

D. Adding and Customizing the Correlation Coefficient Indicator

// Add a Correlation Coefficient indicator

const cc = tradingChart.indicators().addCorrelationCoefficient()

cc.setDataset(dataset)

cc.setPeriodCount(20)

cc.setSymbol('GOOGL')- addCorrelationCoefficient(): This function adds the Correlation Coefficient indicator to the chart. It will be used to analyze the relationship between the two datasets (GOOGL and MSFT stock prices).

- setDataset(): This sets the dataset on which the correlation coefficient is calculated. In this case, it uses the GOOGL dataset.

- setPeriodCount(): Specifies the period for calculating the correlation coefficient. In this case, it uses a 20-period correlation.

- setSymbol(): This sets ‘GOOGL’ as the main stock symbol to be used in the correlation coefficient calculations.

E. Setting the Currency for the Chart

})

tradingChart.setCurrency('USD')

})- setCurrency(‘USD’): This sets the currency of the chart to USD, ensuring that the pricing data is interpreted and displayed in US dollars.

Advantages and Limitations of Correlation Coefficient Statistics in Trading Strategies

Advantages

- Risk Measurement: A statistically significant correlation coefficient can help traders diversify their portfolios. By investing in assets with a low or negative correlation, they reduce exposure to market volatility.

- Strategy Refinement: Traders can develop or refine strategies by examining the correlation coefficient statistical significance between different assets, improving decision-making during times of market uncertainty.

Limitations:

- No Causation: Just because two variables are correlated does not mean one causes the other. Correlations may be influenced by a third variable. For example, ice cream sales and crime rates are correlated, but the actual cause is temperature.

- Outliers Impact: Outliers, or data points that deviate significantly from the rest of the data, can distort the correlation coefficient, making the relationship appear stronger or weaker than it actually is.

- No Effect Size: Correlation measures the strength of a relationship but doesn’t indicate how much one variable affects the other.

- Only Linear: Correlation only captures linear relationships, meaning it may not be suitable for data with non-linear patterns.

Conclusion

Understanding the importance of correlation coefficient in statistics for financial analysis is vital for creating robust trading strategies. This metric allows traders to quantify relationships between assets, helping them optimize portfolios, manage risk, and capitalize on market trends.

Through the integration of tools like LightningChart JS Trader, the power of correlation coefficient statistics is enhanced, offering traders real-time insights and visualizations. However, traders must remember that while the correlation coefficient is a powerful tool, it is most effective when used alongside other technical and fundamental analyses.

By mastering the application and interpretation of the correlation coefficient statistics, traders can better navigate the complex world of financial markets.

Ahmad Omid

Data Science Developer

Continue learning with LightningChart

Best DevExpress Charts Alternative in 2026: GPU Performance for Web and Desktop

DevExpress is one of the most comprehensive UI component suites in the .NET and web ecosystem. WinForms, WPF, ASP.NET, Blazor, JavaScript it covers the full Microsoft-aligned development stack with grids, schedulers, form components, reporting, and charting all...

Best Chart.js Alternatives in 2026: When You’ve Outgrown the Basics

Chart.js is the correct answer for a lot of chart projects. MIT license with no commercial restrictions, ~14KB gzipped, documentation that is genuinely among the best in the ecosystem, 65,000+ GitHub stars, and the largest community of any JavaScript chart library by...

Best AnyChart Alternatives in 2026: GPU Performance, Transparent Pricing, Free Trials

AnyChart is a commercially-oriented JavaScript charting library that markets itself on enterprise reliability, used by over 75% of Fortune 500 companies per their own claims, with a broad catalog of 70+ chart types covering Gantt, maps, stock charts, and more. The...

If you have any questions, feel free to contact us!

©LightningChart Ltd 2026. All rights reserved.